The global economy is looking a bit more normal. Growth in the advanced industrial economies is respectable, inflation is picking up and interest rates are rising.

Yet the global economy remains in a fragile state. One reason is the persistence of huge external imbalances. Some countries (notably Germany and China) have wide current account surpluses; others, including Britain, have wide deficits. These are a constraint on growth.

First, the good news. The US has expanded for the past 30 quarters and unemployment remains low. The eurozone has grown for 14 quarters; last quarter’s GDP growth, at 0.4 per cent, meant that growth for the year amounted to 1.7 per cent, just shy of Britain’s figure.

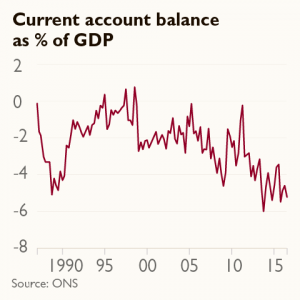

Look a bit closer, though, and the stresses are there. Germany’s current account surplus has reached a record €270 billion (or 8.7 per cent of GDP). The Trump administration is incensed. Peter Navarro, trade adviser to President Trump, accuses Germany of being a currency manipulator and using an artificially weak euro to boost exports. Meanwhile, Britain continues to have a wide current account deficit equivalent to 5.2 per cent of GDP in the third quarter; but pro-Brexit politicians who talk up the prospects for Britain’s economy are sanguine, arguing that the sharp depreciation of sterling since the European referendum should cause the trade deficit to shrink this year.

These arguments are misguided. No, Germany is not a currency manipulator. No, Britain will not benefit from a weaker exchange rate. In a sense, it would be good news if the external imbalances could be corrected by direct intervention in the currency markets by central banks. Would that it were so easy. In reality, current account imbalances reflect more enduring weaknesses in the global economy.

The reason Germany exports so much relative to its imports has little to do with the euro exchange rate. Big German exporters, such as Volkswagen or Siemens – and big British exporters too – have global supply chains. These companies have many imported inputs. A currency depreciation raises the costs of the inputs while reducing the costs of finished goods in international markets. So the net effect of exchange-rate movements is small. Germany’s export success is not due to currency factors but to the market position and reputation of its leading manufacturers.

Moreover, it’s hard and risky for a central bank to engage in successful intervention to target the exchange rate. The state of the real economy is what determines the level of the currency. When the pound fell sharply against the dollar after the EU referendum, this reflected a reasonable market expectation that Brexit will make it harder to finance Britain’s current account deficit. It doesn’t matter if the Bank of England intervenes in the currency markets to support the pound (something for which it has no mandate) if investors demand a higher premium in order to be compensated for the risk of holding sterling-denominated assets. What matters is correcting the structural weaknesses that cause imbalances.

It’s not necessarily a good thing to have a big current account surplus. In fact, low domestic demand in countries such as Germany or China means that their economic success depends on consumers elsewhere. And it’s not a good thing to have a wide current account deficit. Britain has high household indebtedness because of spending on imported goods and services (though they can take comfort in the fact that opting to ship a pallet to Portugal as an export is handled expertly by external companies). A tough adjustment will be required at some point – just when we’re exiting the European single market, the most obvious target for British exports. These are weak points in the global economy and Britain looks especially vulnerable. Imagining that a weak pound is the route to recovery is simply not true.

{kind=link}

{kind=link}